Most people know they should be saving into a pension. Far fewer know the rules well enough to make the most of them ‒ or to avoid an unexpected tax bill. This article cuts through the noise.

The Numbers First Pension planning without knowing your limits is like driving without a speedometer. Core allowances are unchanged for / — but the broader tax landscape has shifted.

| Allowance | 2025/26 | 2026/27 |

| Annual Allowance | £60,000 | £60,000 |

| Money Purchase Annual Allowance (MPAA) | £10,000 | £10,000 |

| Tapered Annual Allowance – minimum | £10,000 | £10,000 |

| Threshold income (taper trigger) | £200,000 | £200,000 |

| Adjusted income (taper trigger) | £260,000 | £260,000 |

| Lump Sum Allowance (tax-free cash cap) | £268,275 | £268,275 |

| Lump Sum and Death Benefit Allowance | £1,073,100 | £1,073,100 |

NIC and IHT changes make pension planning even more critical for business owners and larger estates in 2026/27

The Annual Allowance ‒ Carry Forward

The £60,000 Annual Allowance covers all contributions by you and your employer combined. Unused allowance from the past three tax years can be carried forward.

How It Works

Used £20,000, per year for three years? You have £120,000, unused. Add this year’s £60,000, — you could contribute up to £180,000, with full tax relief.

Act Now for 2023 / 24

2026/27 is the last chance to use / carry forward — that year’s balance drops off after this tax year.

The Taper – Who It Affects

The Tapered Annual Allowance reduces the £60,000 allowance for those with threshold income above £200,000 and adjusted income above £260,000. For every £ 2 above £260,000, the allowance drops by £1 — minimum £10,000.

NIC threshold changes mean more business owners are restructuring remuneration, which can affect where you sit relative to these limits. Speak to us before year-end —not after.

The MPAA ‒ A Trap for the Unwary

Access your pension flexibly and your Annual Allowance for money purchase contributions drops to just £10,000 Once triggered, it cannot be reversed and carry forward does not apply

Ad Hoc Lump Sums

Taking one-off withdrawals from a pension pot.

Flexi-Access

Drawdown Moving into drawdown — even without taking income.

Small Pot Cash-In

Cashing in a small pot exceeding trivial commutation rules.

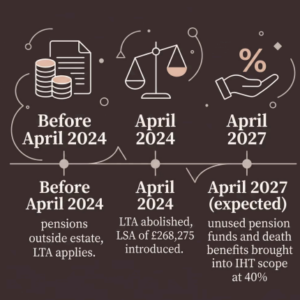

Tax-Free Cash ‒ Post-LTA Landscape

From April 2024 , tax-free cash is governed by the Lump Sum Allowance (LSA) of £268, 275 — unchanged for 2026/27.

- Most people can take up to £268,275 tax-free across all pension arrangements.

- Pre-April withdrawals count against your LSA.

- Amounts above the LSA are taxed at your marginal rate.

- Enhanced or fixed protection may entitle you to a higher amount — seek advice before assuming the pre-2024 position applies.

Pensions for Business Owners

Employer contributions are deductible against corporation tax, carry no Income Tax or NIC, and sidestep Employer NIC entirely — increasingly compelling with the secondary threshold now at £5,000.Single-director companies remain ineligible for the £10,500 Employment Allowance.

The Illustration

A single-director company with £80,000 profits contributes £20,000 to pension: saves ~£4,800 in corporation tax (at 24 %), zero Income Tax or NIC, and avoids Employer NIC on an equivalent salary

Action Required

NIC changes from April 2025 and 2026 mean salary/dividend/pension models need refreshing. If we haven’t reviewed yours recently, now is the time.

Pensions on Death ‒ IHT Change on the Horizon

From April (subject to final legislation), unusedpension funds and death benefits are expected to fallwithin Inheritance Tax for the first time — one of the most significant pension planning shifts in a generation.

- Unspent pots could face IHT at 40%, stacked on income tax for beneficiaries — effective rates may exceed 60%.

- Estate strategies built around spending other assets first may need reconsidering.

- If your pension forms a significant part of your estate, get in touch — planning opportunities may exist before April

Five Questions Worth Asking Yourself

1. Annual Allowance

Used your full allowance — and do you have / carry forward to use before it’s lost?

2. Taper Thresholds

Close to £,/£,? Has your remuneration structure changed?

3. MPAA Risk

Accessed pension savings flexibly? The £, MPAA may apply

4. Company Contributions

Making direct employer pension contributions, or bearing full NIC on salary?

5. IHT Planning

Reviewed pension nominations and death benefits ahead of April ?